⬇️

⬇️

Key Takeaways

- Helion Energy is pushing toward a 2028 fusion deployment for Microsoft as AI load growth stresses U.S. grids

- Zap Energy expands into fission to create a nearer-term revenue path while continuing fusion R&D

- Analyst data shows data center power demand rising sharply, prompting interest in advanced nuclear options

Helion Energy is moving at an unusually fast clip as it works toward delivering fusion-generated electricity to a Microsoft data center in Central Washington by 2028. The pace is not happening in a vacuum. AI infrastructure has turned into one of the most power-hungry buildouts in modern industrial history, and many operators are reaching the limits of what local grids can realistically supply.

U.S. data centers already consumed more than 4% of national electricity in 2023, according to the MIT Energy Initiative. Their forecast suggests consumption could climb to 9% by 2030. Growth at that scale has created a gap between what hyperscalers want and what utilities can deliver on modern timelines.

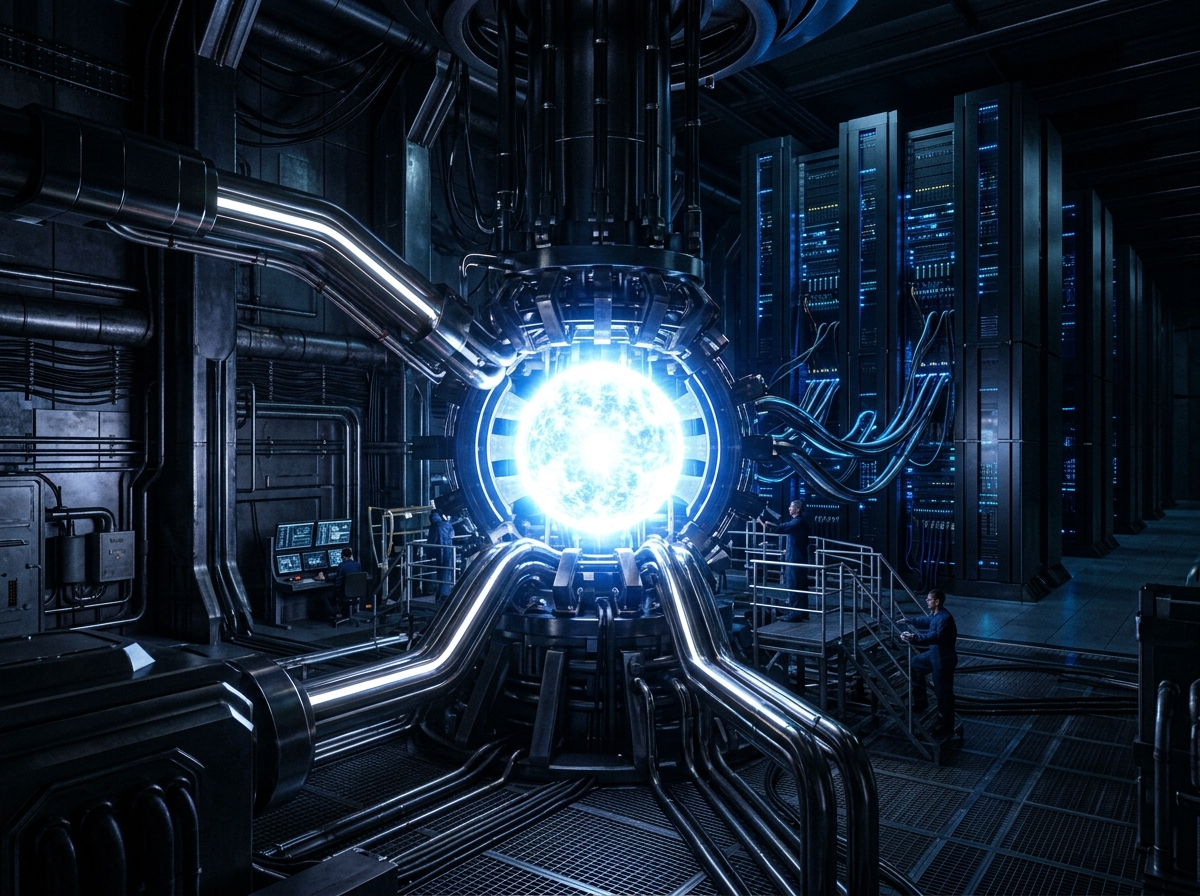

That context helps explain why Helion Energy secured a $1.5 billion war chest and why it signed an unprecedented agreement to sell fusion energy to Microsoft. The company is sprinting to reach its 2028 deadline to flip the switch on the power plant. The timeline creates pressure, but it also creates focus. At Helion’s Everett, Wash., R&D space, the company operates Polaris, a 60-foot-long, seventh-generation prototype that uses magnets to compress plasma, launching and merging it at 1 million miles per hour. The team also built Tiny Merge, a device one-eighth the size of the prototype, which serves as a testbed for faster iterations of its designs.

Power demand forecasts from financial analysts frame why these experiments are getting funded so quickly. Goldman Sachs Research estimates that data center electricity requirements will accelerate 175% by 2030 versus 2023 levels. They also note that private capital for advanced nuclear technologies has increased 13 times compared to 2023. Investors are spreading their bets across nuclear fission, fusion, and hybrid approaches rather than relying on a single pathway.

Meanwhile, the reality on the ground for operators is already complicated. Deloitte has projected that U.S. AI-driven data center demand could reach 123 gigawatts by 2035, up from just 4 gigawatts in 2024. That scale invites a simple question: Where does all that power come from? Transmission queues in the United States are stretched, sometimes requiring five to seven years for new connections. FTI Consulting has warned that global data center demand could hit 71 gigawatts by 2027, and U.S. demand could nearly double to 17 gigawatts in that same timeframe. Operators know they need firm, low-carbon energy, and they need it soon.

Just a few minutes down the road from Helion sits Zap Energy, which is taking a more cautious, diversified approach. The startup has raised $330 million and secured Department of Energy backing. Zap uses a Z-pinch approach, relying on the magnetic field generated by an electrical current to confine plasma. Their FuZE Q device produces a lightning-like plasma strand roughly 2 feet long. When fusion events occur, neutrons transfer heat into a liquid metal blanket before the system converts that heat into power.

However, Zap Energy acknowledges the uncertainties around commercial fusion timelines. The company recently announced it will jointly pursue nuclear fission as a near-term revenue source and a hedge on its fusion bet, developing a 10-megawatt microreactor. Zap's leadership notes this is not a pivot, but rather a strategy to integrate both technologies to move faster, reduce risk, and build a more enduring company. One of their technical arguments is that both fission and fusion benefit from similar liquid metal expertise. Sodium cooling in fission reactors behaves similarly to bismuth and lithium in Zap’s fusion design.

Commonwealth Fusion Systems is another notable competitor in this landscape, with nearly $3 billion in funding. Their plant planned for Virginia places them near the country’s densest cluster of data centers. Companies like TAE Technologies, Avalanche Energy, and General Fusion round out a global cohort of entrepreneurs trying to harness the power of the sun, joining a sector that has more than 50 private ventures globally. China is also pouring large sums into domestic development, although those investments are less transparent.

The policy and interconnection picture is still evolving. Grid integration for any of these technologies will need to meet IEEE power quality and interconnection standards. Many developers are also incorporating AI systems to help manage load planning and dispatch, which brings NIST’s AI Risk Management Framework into view. It is not unusual to see AI models used to balance fusion pulse cycles, campus battery storage, and grid imports. Operators like Microsoft want those systems, but they expect regulatory clarity as well.

Not every scientist believes commercial fusion is around the corner. Some argue that cost-competitive devices remain decades away. Others, including leaders at the Princeton Plasma Physics Laboratory, describe the field as very close to a meaningful breakthrough while still facing substantial hurdles. That tension makes the sector unusually dynamic. It also explains the range of strategies, from Helion’s sprint toward a 2028 commercial milestone to Zap’s hybrid fission and fusion play.

For hyperscalers, the appeal is straightforward. AI workloads keep growing, and many regions are restricting new data center development because local communities are worried about power access and water usage. Fusion offers the possibility of compact, non-emitting, high-capacity plants located near large campuses. Whether the technology arrives in time is unclear. Yet the pressure on the grid is so strong that end users are willing to engage earlier than they would have in past energy cycles.

Some of these companies may not hit their dates, and some prototypes may be reworked several times. That said, the incentives have never aligned quite like this. Data center operators need firm power, investors are willing to fund multiple pathways, and fusion developers see a defined market with urgent demand. The next few years will determine whether this moment becomes a long-term energy shift or a brief detour in the broader search for reliable clean power.