⬇️

⬇️

Key Takeaways

- Igneo Infrastructure Partners acquired a portfolio of seven data centers

- The deal reflects continued investor demand for digital infrastructure assets

- Capacity, power availability, and regional diversification remain critical factors for operators and buyers

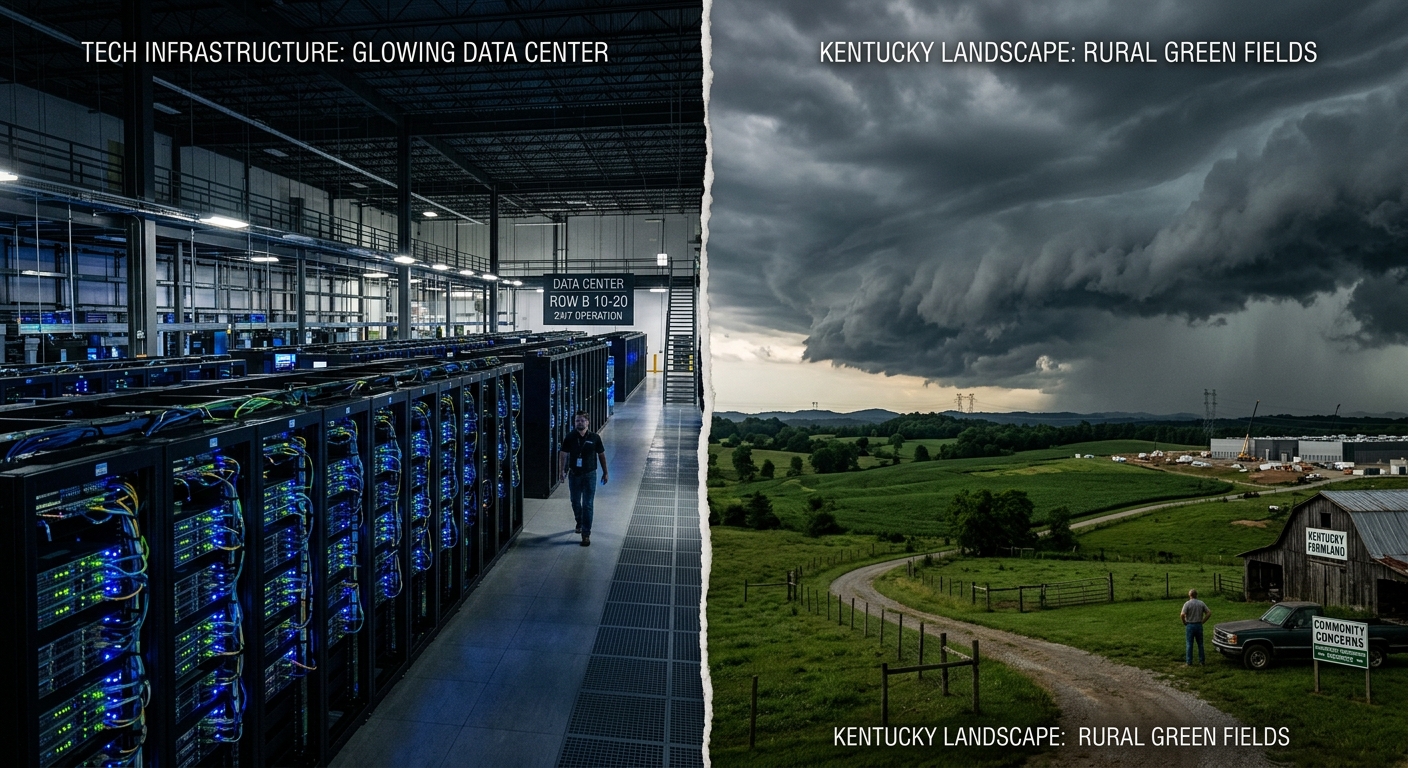

Global infrastructure investment manager Igneo Infrastructure Partners has acquired a portfolio of seven data centers. The data centers include a mix of facilities serving enterprise and cloud workloads, though the full composition was not publicly detailed. Even so, the move fits into a broader pattern: institutional capital continues to flow steadily into digital infrastructure, often faster than operators can build it.

Data centers are no longer a niche asset class. They have shifted into the mainstream for infrastructure investors seeking predictable cash flows tied to long-term digital demand. This demand shows no signs of slowing. Cloud adoption continues, AI workloads are expanding, and enterprises are consistently shifting from on‑premise IT footprints to colocation and cloud hybrids. The acquisition is more than a simple portfolio addition; it is another signal that investors see resilience in the sector.

Not every deal lands with the same rationale. Some buyers seek scale, others geography. Occasionally, the primary driver is power access. In this case, Igneo Infrastructure Partners is leaning further into a sector where capacity shortfalls are increasingly common. Many operators are currently dealing with power availability bottlenecks, especially in high‑density urban zones. Growth in AI clusters only tightens those constraints, making existing facilities—particularly those already energized—highly valuable.

Interestingly, investor activity like this often prompts questions about whether consolidation ultimately helps or hurts enterprise buyers. Does it lead to more standardized pricing, or will scarcity push rates upward? The answer varies by region, but consolidation tends to bring deeper pockets for expansion. That said, expanding power and cooling infrastructure is not trivial. Lead times for substations, transformers, and even basic permitting have stretched in many markets.

It is also worth noting that not all data centers are created equal. Some portfolios lean toward legacy enterprise facilities, while others include more modern hyperscale‑ready builds. Without specifics on the acquired sites, it is difficult to categorize this portfolio precisely. However, any collection of seven operating facilities offers a foundation for modernization. Operators frequently retrofit power distribution systems, cooling, and interconnection capabilities to meet new workload demands. That process can take time, but it offers investors a clear value‑creation roadmap.

Meanwhile, regional diversity has become a strategic asset. Different markets have different utility constraints, talent pools, and fiber availability. A multi‑facility acquisition often gives buyers an immediate footprint they can expand without starting from zero. In some markets, greenfield development has become so time‑consuming that acquiring existing sites is the only realistic path to near‑term growth.

There is also the customer angle. Enterprises increasingly expect hybrid flexibility: some workloads need low latency, while others need cost‑efficient scale. A portfolio spread across varied locations can serve that mix more effectively. While this adds operational complexity, most investors are prepared for it, often partnering with operators who can manage the technical nuances. The industry has matured enough that ownership and operation frequently split, allowing each party to lean into its strengths.

Sustainability pressure is another factor often overlooked in acquisitions like this. Data centers remain under scrutiny for energy consumption, water usage, and emissions. Investors acquiring portfolios today often step into a multi‑year upgrade cycle involving renewable energy procurement, improved efficiency measures, and sometimes the adoption of alternative cooling approaches. These initiatives are no longer optional, as regulatory bodies and enterprise customers both demand progress.

Investments of this scale reflect a long-term view. Even with rising energy costs and supply chain challenges, digital infrastructure has proven consistently stable. Workloads grow even during economic downturns. Additionally, while the hype surrounding AI is loud, it translates into real infrastructure spending. Chipmakers, cloud providers, and enterprises deploying private AI stacks are all feeding into upstream demand for power‑dense facilities.

Looking at the landscape more broadly, private and institutional investors have been steadily expanding their data center exposure for years. Some focus on mature markets; others target secondary regions where land and power remain comparatively available. This acquisition by Igneo Infrastructure Partners aligns with this trend, reinforcing the sector’s continued attractiveness. It may also position the firm to capture upside from modernization cycles, power‑availability improvements, and hybrid cloud expansion.

Ultimately, the deal highlights that stability matters. Seven data centers represent tangible assets with long-term relevance in a digital-centric economy. Investors, operators, and enterprises relying on consistent uptime recognize this value. Whether more acquisitions of this type surface in the coming months remains to be seen, but the demand environment suggests they will. The market remains strong, and capital continues to seek durable assets.